MPT is a mathematical formulation of the concept of diversification in investing, with the aim of selecting a collection of investment assets that has collectively lower risk than any individual asset. This is possible, in theory, because different types of assets often change in value in opposite ways. For example, when the prices in the stock market fall, the prices in the bond market often increase, and vice versa. A collection of both types of assets can therefore have lower overall risk than either individually.

More technically, MPT models an asset's return as a normally distributed random variable, defines risk as the standard deviation of return, and models a portfolio as a weighted combination of assets so that the return of a portfolio is the weighted combination of the assets' returns. By combining different assets whose returns are not correlated, MPT seeks to reduce the total variance of the portfolio. MPT also assumes that investors are rational and markets are efficient.

MPT was developed in the 1950s through the early 1970s and was considered an important advance in the mathematical modeling of finance. Since then, much theoretical and practical criticism has been leveled against it. These include the fact that financial returns do not follow a Gaussian distribution and that correlations between asset classes are not fixed but can vary depending on external events (especially in crises). Further, there is growing evidence that investors are not rational and markets are not efficient.

Concept

The fundamental concept behind MPT is that the assets in an investment portfolio cannot be selected individually, each on their own merits. Rather, it is important to consider how each asset changes in price relative to how every other asset in the portfolio changes in price.

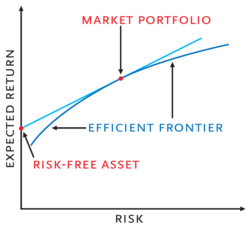

Investing is a tradeoff between risk and return. In general, assets with higher returns are riskier. For a given amount of risk, MPT describes how to select a portfolio with the highest possible return. Or, for a given return, MPT explains how to select a portfolio with the lowest possible risk (the desired return cannot be more than the highest-returning available security, of course.)

MPT is therefore a form of diversification. Under certain assumptions and for specific quantitative definitions of risk and return, MPT explains how to find the best possible diversification strategy.